Download The 2025 M&A Report For Free!

Your download is on the way to your email inbox!

Please make sure your email is typed corectly.

All information is protected & secure.

This is a continuation in our series exploring rollover equity acquisition deals. Part I focused on deal structures from the vantage of acquirors. In Part II we will be diving into what these types of deals mean to the car wash seller.

This is a continuation in our series exploring rollover equity acquisition deals. Part I focused on deal structures from the vantage of acquirors. In Part II we will be diving into what these types of deals mean to the car wash seller.

The first half of 2024 has brought a major and significant slowdown in carwash M&A, along with a stark decrease in the dispersion of acquiring parties. Transaction count is down ~46% and the number of sites sold and acquired is down nearly 40%, both compared to the first half of 2023. By way of most active acquirers, 2024 posted a large increase in deal concentration. Most notably, during the first half of 2023, the most active acquiror by transaction count was El Car Wash, having been the acquiring group in just 11% of the announced transactions. The first half of 2024 had Whistle Express representing a commanding 43% of deals as the acquiring group. In this industry report, we cover all announced M&A transactions in Q2 and provide a candid overview of market trends.

This is a continuation in our series exploring rollover equity acquisition deals in the car wash industry. Part I focused on these deal structures from the vantage of acquirors. Here in Part II we will be diving into what these types of deals mean to the car wash seller.

The truth with any acquisition transaction, especially one that includes a rollover equity component, is that it must be considered on an individual one-off basis. Making gross generalizations as to “equity rollovers are good” or “this is a good offer”, is both dangerous and reckless. However, what is true of all rollover equity acquisitions, is this fundamental truth: The Seller is truly making a second and largely separate investment in a new company (and debatably more importantly – the new operators).

This is best illustrated through a hypothetical example where there are three potential offers on the table.

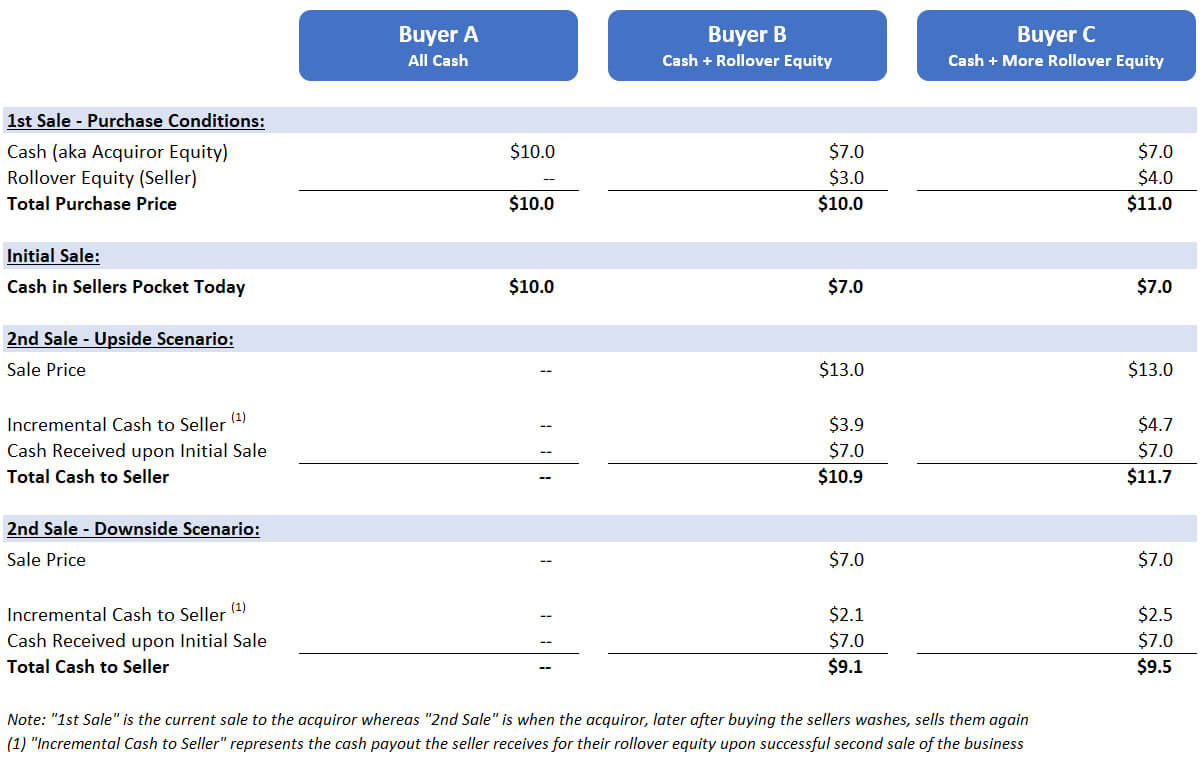

Let’s imagine you own a car wash that currently does $1MM in EBITDA. You have it in your head that you want $10MM for the wash. Let’s assume you were approached by three different buyers, each with their own offer:

In order to meaningfully examine and exemplify the takeaways here, certain assumptions must be set that allow for a true comparison and conclusion(s):

Please Note - “Upside” and “Downside” Scenarios are predicated under the assumption that the seller receives the same class of equity as the general and rest of the equity capital structure of the pro-forma business. This assumption is in the sellers favor and is sometimes not the case. If the seller was to receive a different class of more junior equity – the ‘Downside Scenario(s)’ would be grimmer. During these scenarios, there is a chance the seller would be entitled to no payout at all, coming in as a junior holder with the more senior equity having a preferred payout in what is essentially a “down round”. This would not impact the seller’s payout in the “Upside” scenarios so much but could to some extent dependent on the specific differences in equity classes.

The payout a seller and holder of rollover equity will receive on this component of their compensation will largely be based on the success (or lack thereof) of the resulting company after sale. Success must be defined both in the way both performance and a liquidity event (second sale).

Two different performance scenarios have been painted. Both these make large generalizations to illustrate the different ends of the future possibility spectrum.

This scenario depicts a future where the company is sold again later down the road for even more. This is a simplification of all the moving parts (future acquisitions, margins, valuation metrics, dilution, etc.) but will serve all the same in illustrating the meaningful points. The ‘Upside Scenario’ is the future where the company that you sold is now worth more on a apples-to-apples comparative basis than what it was valued for when you originally sold it. In other words – your “stock price went up."

A treasure trove worth of variables can cause this including accretive acquisitions, multiple expansion, margin improvement, topline growth, etc. But for this discussion, let it suffice to say that the resulting company was successful in increasing the value of what they bought compared to how much they paid. The seller, as an equity holder in this resulting company, is indeed a beneficiary of this increase in value.

What often goes overlooked by many with private investments is liquidity and the ability to realize value. Let’s say that the resulting company ended up buying no additional car washes after buying yours, but increased EBITDA by 10%. That is wonderful but does not mean your equity is worth 10% more. Your equity is worth whatever price someone is willing to pay for it. Which brings us to the second part of how “successful” (and the ‘Upside Scenario’) is defined – the ability to achieve a liquidity event at this favorable valuation. As mentioned, this secondary liquidity event will most likely be when the resulting company sells itself to another larger acquiror in the space.

In conclusion, the ‘Upside Scenario’ depicts a future where the company you sold is sold again for even more later.

Not all companies are more successful, or successful at all, after being acquired. The ‘Downside Scenario’ is simply defined as a future where the acquiror of your company ends up later selling the company for less than what they originally purchased it for from you. This can happen for pretty much all the reverse reasons that can cause the ‘Upside Scenario’.

Rollover equity holders don’t just share in future upside and success, but also future downside and failure. The downside scenario depicts a future where your “stock price went down”.

When a car wash is sold for all cash, with no contingencies or deferred payouts, it’s simple. The seller gets paid and gets all of it on close. This is our “plain vanilla” control group for this examination and exploration.

In this scenario, the buyer is offering 10x EBITDA resulting in a total purchase price of $10MM. The seller receives all of this.

Buyer B - Lesson: Equity ≠ Cash

Buyer B brings to the table a total purchase price of $10MM – which will undoubtably be pitched as buying the company for 10x (which is not wrong). But this is different than receiving 10x for the wash in all cash up front. As Buyer B is proposing a $3MM slug of rollover equity as a portion of that $10MM total purchase price.

As per the assumptions, equity stakes are proportional to post money valuation, with no difference in seniority or security class, resulting in a 30% ownership stake in the pro-forma company ($3MM ÷ $10MM).

In this scenario the resulting company ends up being sold in the future to a second buyer for 30% more than it was bought for. The original seller, as an equity holder, is indeed a beneficiary who now sees the gains from their successful and savvy investment – resulting in an extra ~$900K (30% increase in $3MM of rollover equity) than the seller would have received in total from Buyer A (who paid all cash up front). However, the $3.9MM the seller receives on the backend is after an uncertain amount of time and is not received on the day of sale.

In this scenario, the resulting company does experience a liquidity event through a second sale but sells for less than the post-money “total value” it was originally purchased for. Put simply, you are a stock holder, and the stock price has gone down. Commiserate with such, the seller sees their $3MM of rollover equity now being worth $2.1MM (down 30% from the value attributed to the equity when they originally sold). In this future, the seller ends up with $7MM in their pocket on the day of original sale, and $2.1MM incremental at an undetermined date in the future when there is a second liquidity event. This results in the seller receiving a total of $9.1MM for their car wash.

The Buyer B comparison paints this crucial point; a seller’s payday in the form of rollover equity is completely and totally dependent on the future success of the resulting company (and the team leading that future company). The seller shares in both the future success upside and the future failure downside of the company, and the seller has opted to give up value today for a variable future payout.

Buyer C throws a new wrench into the equation; higher total purchase price. Along with this higher purchase price comes a larger proportion of rollover equity. Buyer C is not offering 10x EBITDA, but rather 11x EBITDA, creating a total purchase price of $11MM. However, the cash portion of compensation on close is $7MM (same as Buyer B), with the remaining now $4MM being in rollover equity.

In this scenario, the resulting company successfully finds a secondary liquidity event where on a comparable and all-else-equal basis, the resulting company’s value has increased to $13MM (same as the ‘Upside Scenario’ for Buyer B). In this scenario, again, as an equity holder in the company, the original seller is a beneficiary of this success. This time however, the magnitude of impact on their total payout is increased due to the larger proportion of rollover equity. The seller ends up with a total of $11.7MM ($7MM cash on original sale and an additional $4.7MM at a future date from the rollover equity portion).

This sounds great, but on second look, the natural question arises – why is the seller only up ~18% on their rollover equity portion and not 30%? This is a very astute, relevant, and important observation. For now, the short answer is because by purchasing the car wash for more in the beginning, the acquiror has devalued the expansion / profit experienced between when they bought the wash and when they sell the company during the second liquidity event. Remember, the acquiror didn’t pay $10MM like Buyer B. They so generously paid $11MM. So, the company only experienced a $2MM (as opposed to $3MM) value increase when reaching secondary liquidity at a $13MM sale, which is no longer a ~30% increase.

Here, same as with the Buyer B ‘Downside Scenario’, the resulting company ends up being sold for $7MM later down the road. Just as positive returns were amplified by the larger proportion of rollover equity compensation in the ‘Upside Scenario’, so is the opposite true in this ‘Downside Scenario’ here. The “stock is down” again. But this time, the seller owns more stock. The sellers total end of the day compensation after the secondary liquidity event is $9.5MM total ($7MM of upfront cash upon initial sale, and $2.5MM for the rollover equity upon the secondary sale later).

Buyer C is both the most interesting and pertinent. Here we have a buyer who has come to the table with an offer higher than all others. Buyer C is willing to buy the car wash for 11X (aka $11MM) which is a full $1MM higher than everyone else. This may seem flattering, as they are willing to pay the most. However, there is a very possible future (the ‘Downside Scenario’) where the seller ends up only making a total of $9.5MM. This should be held in stark contrast to the scenario and payout of Buyer A. Buyer A offered you a full $1MM less than Buyer C, but there is a future where by going with Buyer C’s higher offer, the seller makes less money.

A higher “total purchase price” or “total offer” does NOT mean that the seller always makes more money.

There are two major points that should be taken away here:

A seller that accepts part of their compensation as rollover equity is essentially investing in a different company. Even if the seller stays onboard in a large capacity, they will no longer be calling all the shots. This introduces an immediate and real aspect and element of uncertainty (both in time and performance) that should not be ignored. Whether it is a new private equity entrant that is acquiring washes as their first purchase (from which they will presumably build upon through future additional bolt-on acquisitions) or whether the washes are being acquired by a current active player in the space that already owns 20 washes, the seller is not investing in just their washes. The seller is in fact investing in the resulting total company. This cannot be stressed enough. And this is true for better or worse.

When a company is bought for a very high value, and the initial seller has part of their payment tied to the buyer’s ability to go and sell it again to someone else for more – this creates uncertainty and risk. The higher the price the company is originally bought for, the harder it is to sell that same company for even more later.

This article has undoubtably painted equity rollover deals in an overarchingly negative light. This is both not my intent, and not the truth. Many times, these deal structures do succeed in both aligning incentives, and providing additional upside potential to the seller. Please do not walk away from this article with the takeaway belief that all equity rollover deals are bad. Equity Rollover deals can be stellar for both sellers and acquirors.

I so often receive questions on these deal structures, and I am never worried about the upside being great. When it works – it can work wonderfully and everyone (especially the seller) truly does win. What is worth talking about is both how to truly understand what these deals are, and what to be aware of.

This article was created to hopefully do this; to allow you to understand why private equity and outside acquirors prefer this deal structure, what’s in it for them, and what it means for the sellers. Equity rollover deal structures are the same as any other risk / reward trade-off; it’s a tradeoff. It is up to the seller to determine whether the tradeoff is one you are willing and wanting to make.

Car Wash Advisory founder Harry Caruso joins Wash Talk to discuss slowing transaction volume, buyer activity and the outlook for car wash M&A in 2026.

The Definitive Quick Guide: Created and Written by Car Wash Advisory Team