Download The 2025 M&A Report For Free!

Your download is on the way to your email inbox!

Please make sure your email is typed corectly.

All information is protected & secure.

Is Mister Car Wash a take-private candidate? Explore valuation compression, private vs. public market dynamics, and lessons from Dentalcorp’s public-to-private journey.

Is Mister Car Wash a take-private candidate? Explore valuation compression, private vs. public market dynamics, and lessons from Dentalcorp’s public-to-private journey.

The first half of 2024 has brought a major and significant slowdown in carwash M&A, along with a stark decrease in the dispersion of acquiring parties. Transaction count is down ~46% and the number of sites sold and acquired is down nearly 40%, both compared to the first half of 2023. By way of most active acquirers, 2024 posted a large increase in deal concentration. Most notably, during the first half of 2023, the most active acquiror by transaction count was El Car Wash, having been the acquiring group in just 11% of the announced transactions. The first half of 2024 had Whistle Express representing a commanding 43% of deals as the acquiring group. In this industry report, we cover all announced M&A transactions in Q2 and provide a candid overview of market trends.

What would happen if Mister Car Wash (NASDAQ: MCW) – the largest operator in the United States and the sector’s only public benchmark – went private?

The implications would extend far beyond a single ticker symbol.

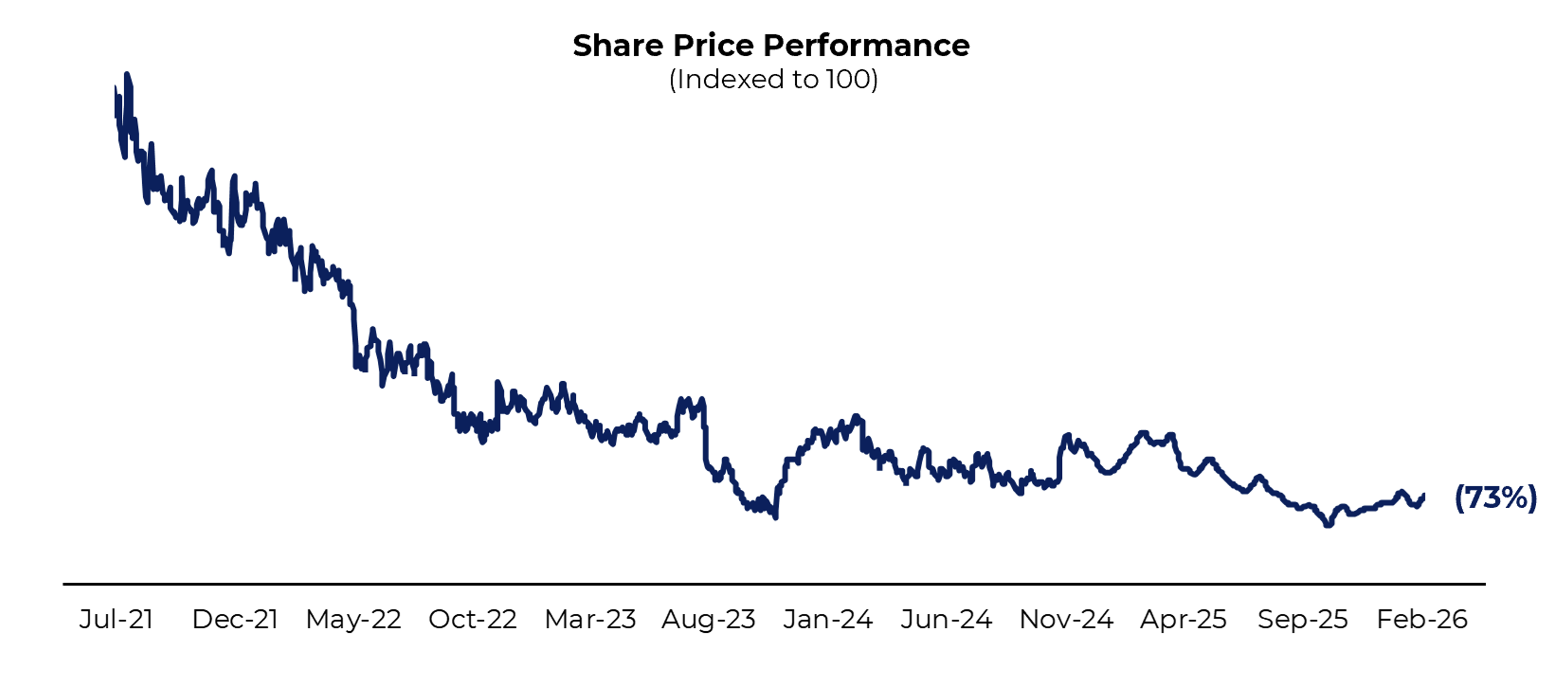

MCW’s stock price has fallen by more than 70% since its June 2021 IPO and remains down ~20% year-over-year. The firm has yet to fully achieve its original growth objectives or realize expected cost synergies and economies of scale – and its market valuation has reflected that gap.

Over the last five years, Mister has added well over 100 sites, primarily through greenfield developments (~75%), increasing its tally to 520+ locations. During the same period, the company has continued to grow membership subscriptions, which now account for over 75% of revenue. When MCW went public, it was trading at a ~25x EBITDA. The multiple has since compressed to approximately 7-8x, materially impacting M&A activity, capital raises and debt refinancings in the private market.

The disconnect between operating progress and public equity performance has become increasingly visible, and share price drift has materially impacted private market valuations and transaction volume. In many ways, private markets are stuck holding their breath for Mister to either be taken private or rebound to what many view as an appropriate valuation multiple and associated share price. The irony is clear: Mister may be better suited as a private company – yet at today’s valuation, it remains too expensive to take private, with no clear near-to-mid-term catalyst for meaningful share price movement.

When Mister went public, the car wash industry was marketed as a growth-oriented story for a national player, with the tailwind predicated on the existence of national scale synergies and increasing operating leverage. This is particularly true for a historically acquisition-driven company (as opposed to new-development-focused), such as MCW. The rising valuation multiples in the 2018 – 2022 private equity surge in the industry forced Mister to reevaluate and pivot.

MCW’s public performance reflects this tension. Despite continued membership growth and site expansion, the market has repriced the company amid rising interest rates and broader multiple compression across the automotive aftermarket.

One could argue that Mister is significantly better suited as a private company, for reasons such as:

Private ownership allows execution of 3–5 year plans without the volatility of quarterly earnings reactions. Multi-year initiatives – price optimization, membership penetration and geographic clustering – are far easier to implement without public scrutiny.

Sponsors can recapitalize, refinance or lever assets in ways that optimize return profiles.

A private sponsor can aggressively optimize pricing, restructure underperforming units and invest in brand positioning without worrying about quarterly same-store sales optics.

Compensation flexibility improves under private ownership. Equity-heavy packages for top operators, regional managers and integration teams can align incentives more directly with long-term value creation

This dynamic eerily resembles another high-profile roll-up strategy that struggled in the public markets before ultimately being taken private.

Dentalcorp (formerly TSX: DNTL) is the largest Dental Support Organization in Canada, operating a network of ~575 of the 15,000 dental clinics in the country. This is strikingly similar to MCW’s market share of express exterior washes in the United States. Much like the car wash industry over the last several years, DSOs have been one of the hottest acquisition targets for private equity. DNTL grew from 10 dental practices in 2011 to over 450 in 2021 before its IPO. The company had previously received large investments from Imperial Capital (GO Car Wash sponsor) and L Catteron. After going public, shares underperformed materially, with public markets questioning growth durability and margin sustainability. The stock price fell by nearly 50% before GTCR, another large private equity sponsor, agreed to a take-private in September 2025 at a 33% premium to current trading levels.

The lesson: public markets are not always patient with roll-up stories that require significant capital deployment, integration and densification to fully mature, especially when they are predicated on significant growth and synergies that aren’t realized.

Another shared characteristic to Mister: Dentalcorp was the only public player operating in a historically fragmented industry with episodic M&A activity. They also grew strictly through acquisitions and had real estate optionality, though they relied heavily on sale-leaseback proceeds. Synergies from scale proved limited, primarily confined to dense geographic clusters.

KKR invested in 123Dentist, the second largest DSO in Canada for ~17x EBITDA in 2022 – far above the DNTL market price. This acquisition is very comparable to private transactions in the last few years in the car wash space, like KKR’s investment in Quick Quack.

The resemblance is uncanny and the car wash industry may be approaching a similar inflection point. Dentalcorp IPO’d at ~15x EBITDA, before trading around 9x and a take-private near 11x. Is MCW cheap enough to warrant a comparable transaction and premium?

If MCW is taken-private, how might sponsors drive incremental value?

In theory, and in accordance with common practice and belief, there are historically five main strategies:

1. Same‑Store Sales Optimization

2. Accelerated M&A Roll-Up

3. De‑Novo Growth / Greenfield Developments

4. Real Estate Monetization (Sale‑Leasebacks)

5. Geographic Densification

In truth, none of these are viable for Mister Car Wash.

A more unconventional strategy – building upon geographic densification – is needed to extract significant value from a potential take-private: Portfolio Segmentation

In a recent poll, nearly every consolidator stated that they search for acquisitions where there is a clear path to being a top operator in the market.

The outcome: “Super-regionals” are a much more likely result of a MCW take-private and the next consolidation curve in the ever-dynamic car wash industry. Regional groups could look to build density and new private equity entrants could see a clear path to being the top operator in attractive markets.

However, this process could take years to accomplish and would dominate the buy-sell landscape. The key question is whether MCW is cheap enough to enable direct regional multiple arbitrage. At current trading levels, the math simply does not support the transaction.

.png)

Harry Caruso recently contributed to an industry article that looks at where the market stands today. While deal activity has cooled, profitability and long-term growth remain strong.

Our Top Companies and Top Acquisitions pages have become trusted resources across the car wash industry. We’re inviting the community to help keep these tools accurate and up to date.